Dit is de webversie van editie 3, 23 april 2023, van mijn wekelijkse nieuwsbrief, aanmelden kan hier.

De afgelopen dagen stond Amsterdam heel even centraal in de online wereld en het had niets te maken met Ajax. Het deed me terugdenken aan 2003, twintig jaar geleden.

Op het Leidseplein in Amsterdam stond toen een groepje onbekende Amerikaanse comedians op het podium bij Boom Chicago, het comedy theater dat het vooral moest hebben van dronken toeristen. In Californië werd onder hoongelach de eerste iLife-suite gelanceerd, bestaande uit ondermeer het logge iTunes en iDVD waarmee je heel traag DVD’s kon branden, door het zieltogende Apple. Steve Jobs stond ruim 5 jaar aan het roer en op een omzet van $6 miljard dollar was Apple verlieslijdend.

De onverwachte ster van Ted Lasso, Hannah Waddingham, geeft in de aflevering Sunflowers kale mannen hoop

Wie toen had voorspeld dat twintig jaar later een briljante comedyshow die is gebaseerd op een goedkope commercial, gemaakt door deze comedians, op een streaming service van Apple allerlei records zou breken met liefst 52 Emmy Award-nominaties, zou direct voor gek zijn verklaard. Ted Lasso, het geesteskind van Boom Chicago alumni Jason Sudeikis, Brendan Hunt en Joe Kelly, won twee jaar achtereen de Emmy Award voor beste comedyserie. Eerder won Apple TV+ als eerste streaming dienst een Oscar voor beste film, met CODA, wat leidde tot een sterke groei in het aantal abonnees van Apple TV+.

Het is appels met aardappels vergelijken, maar het is aardig om te bekijken hoe een ander legendarisch bedrijf dat liefst alleen hardware wilde maken en geen content, het in dezelfde periode is vergaan: ons eigen Philips maakte in 2003 in tegenstelling tot Apple wel winst, zelfs bijna €500 miljoen op een omzet van €29 miljard, bijna vijf keer zoveel omzet als Apple dat jaar. Twintig jaar verder is Philips €15 miljard waard op een omzet van €17 miljard en heeft Apple een marktwaarde van €2.3 biljoen. Vergeet al die nullen: dat is 2300 keer een miljard. Apple is in twee decennia ruim 150 keer zoveel waard geworden als Philips en is op weg naar een jaaromzet van ruim $500 miljard, waarvan alleen al $100 miljard afkomstig uit de services-divisie. Niet slecht voor een bedrijf dat tot woede van Steve Jobs zo slecht was in services, dat het nog geen fatsoenlijke email-dienst kon leveren. Of heeft er nog iemand een MobileMe-adres?

Maar ik dwaal af, want geheel in de geest van Ted Lasso wil ik graag positief zijn deze zondag. De aflevering van afgelopen woensdag, Sunflowers, was de reden dat ik moest terugdenken aan de periode waarin de creatieve geesten achter Ted Lasso in Amsterdam woonden. Sunflowers is een ruim een uur durende lofzang van de makers aan Amsterdam. Inclusief André Hazes en zelfs een flard Rob de Nijs. Het enige ongeloofwaardige moment van deze aflevering was het begin, de 5-0 overwinning van Ajax in de Johan Cruijff Arena. Terwijl in werkelijkheid het enige scorende team van Ajax het mediateam was, dat een grote banner ontvouwde op de pub in Londen waar een deel van Ted Lasso wordt opgenomen.

Waarom is een Amsterdamse ‘vector database’ 200 miljoen waard?

Wie zou niet lachen?

Waar alle hoofdrolspelers van Ted Lasso in de Amsterdamse aflevering een richting bepalende doorbraak beleefden, gold hetzelfde voor een mij onbekende startup die bekend maakte liefst $50 miljoen te hebben opgehaald in de derde financieringsronde. Weaviate noemt zichzelf een ‘vector database’ maar als laatste generatie bij wie wiskunde niet in het verplichte vakkenpakket zat, ben ik daarmee niet verder geholpen. (Ik gok dat de naam staat voor weav-iate, doe iets met weven, en niet voor we-aviate, wij vliegen). Zoekend naar meer informatie over Weaviate, tot januari nog SemI genaamd hetgeen niet meer inzicht verschaft, vond ik deze uitstekende uitleg van CEO Bob van Luijt:

‘De databasetechnologie van de eerste generatie wordt vaak aangeduid met het acroniem SQL […] die conceptueel vergelijkbaar zijn met spreadsheets of tabellen. In de jaren tachtig werd deze technologie gedomineerd door bedrijven als Oracle en Microsoft. De tweede golf databases wordt “NoSQL” genoemd. Deze zijn het domein van bedrijven als MongoDB (en Elastic, MF). Ze slaan gegevens op verschillende manieren op […] maar wat ze allemaal gemeen hebben is dat het geen relationele tabellen zijn. […] De derde golf databasetechnologieën richt zich op gegevens die eerst door een machine-learningmodel worden verwerkt, waarbij de AI-modellen helpen bij het verwerken, opslaan en doorzoeken van de gegevens, in tegenstelling tot de traditionele manieren.’

Dat is een prima uitleg en het is slim om Weaviate zo te framen. Zonder het te zeggen impliceert Van Luijt dat Weaviate een enorm groot probleem oplost in een enorme markt, muziek in de oren van investeerders, verwijzend naar een aantal branchegenoten waarvan de ‘kleintjes’ zelfs beursgenoteerd zijn en een marktwaarde hebben van $16 miljard (MongoDB) en een kleine $6 miljard (Elastic). Alleen zijn die van de oude generatie, lispelt Van Luijt eigenlijk tussen neus en lippen door, en Weaviate is beter.

Een paar dingen vallen me op:

- $50 miljoen op een waardering van $200 miljoen is een hoog bedrag voor een relatief lage waardering. Dat klinkt absurd, maar bedenk dat Character.ai een paar weken geleden $150 miljoen ophaalde op een waardering van ruim een miljard. Toch is deze funding een verstandige beslissing van Weaviate, want het blijft een feit dat Amerikaanse vc’s in niet-Amerikaanse bedrijven minder geld investeren, en tegen lagere waarderingen, dan in Amerikaanse bedrijven. Om in Ted Lasso-sferen te blijven: een Engelse Premier League Club betaalt nu eenmaal meer voor een speler van een andere Premier League Club, dan voor Jan Maas uit de Eredivisie. (Dat karakter dat altijd de waarheid spreekt, hoe pijnlijk soms ook, is overigens genoemd naar Saskia Maas, de CEO en drijvende kracht achter Boom Chicago.)

- in totaal heeft Weaviate nu $67.7 miljoen opgehaald binnen drie jaar en daarmee kan het bedrijf meedoen in de ontwikkeling van fundamentele technologie voor een internationale markt. Wat Weaviate doet is vergelijkbaar met het spelen van Champions League voetbal met een Nederlandse club. Gelukkig hebben Van Luijt c.s. nu voldoende middelen om goede spelers aan te trekken. (Dit is de laatste voetbalvergelijking.)

- ING nam al deel in de A-ronde van 2022 want het kende Weaviate, als spin-out van ING Labs. Het is te prijzen dat een traditionele grootbank als ING een dermate risicovolle investering deed, mits de bank ook daadwerkelijk met de technologie van Weaviate aan het werk gaat. Anders is het een normale venture capital investering en die scoren in Nederland gemiddeld niet beter dan de AEX-index. Overigens geestig dat de naamsverandering van Weaviate is voorbij gegaan aan de beheerder van de portfoliopagina van ING Ventures. Daar heet het bedrijf nog gewoon SemI.

- Alex van Leeuwen nam deel aan de seed-ronde van Weaviate en deed daarmee wellicht één van de beste investeringen ooit in Nederland. Investeerder Peter Thiel kocht in 2004 een belang van 10% in Facebook voor $500.000 en verkocht zijn belang voor in totaal ruim $1 miljard, zover bekend de best renderende investering in venture capital. Zo vrolijk (2000 x) zal het misschien niet worden voor Van Leeuwen, maar ik sluit het niet uit. Databasebedrijven, dat hebben we geleerd aan die oudjes uit de eerste en tweede generatie, kunnen relatief eenvoudig snel opschalen zonder enorme vervolginvesteringen.

Fijne links

- Het FD publiceerde dit grondige artikel over Lightyear met de kop ‘hoe het knuffelbedrijf van Nederland op een haar na ten onder ging.’ De desinteresse van buitenlandse technologie-investeerders in Lightyear (vergelijk het met Weaviate) had een teken aan de wand moeten zijn.

- Meestervlogger Casey Neistat maakte met opzet een vreselijke vlog op basis van een script geschreven door ChatGPT4. Zijn conclusie: AI mist ziel, mist diepte. Ik denk dat ChatGPT4 op dit moment vooral context mist, want nog niet gevoed met Casey’s verleden, perspectief en toon.

- ChatGPT’s CTO Greg Brockman gaf deze fascinerende presentatie over de mogelijkheden van ChatGPT, die zoveel verder reiken dan wat ’tekst en plaatjes’ vragen. Het interview met TED-oprichter Chris Anderson direct na de presentatie is ook verhelderend. Dank aan Michiel Schoonhoven van contentmarketing-specialist NXTLI voor de tip.

Spotlight 9

(ChatGPT4 bedacht deze rubrieksnaam, zie de p.s. onder deze nieuwsbrief.)

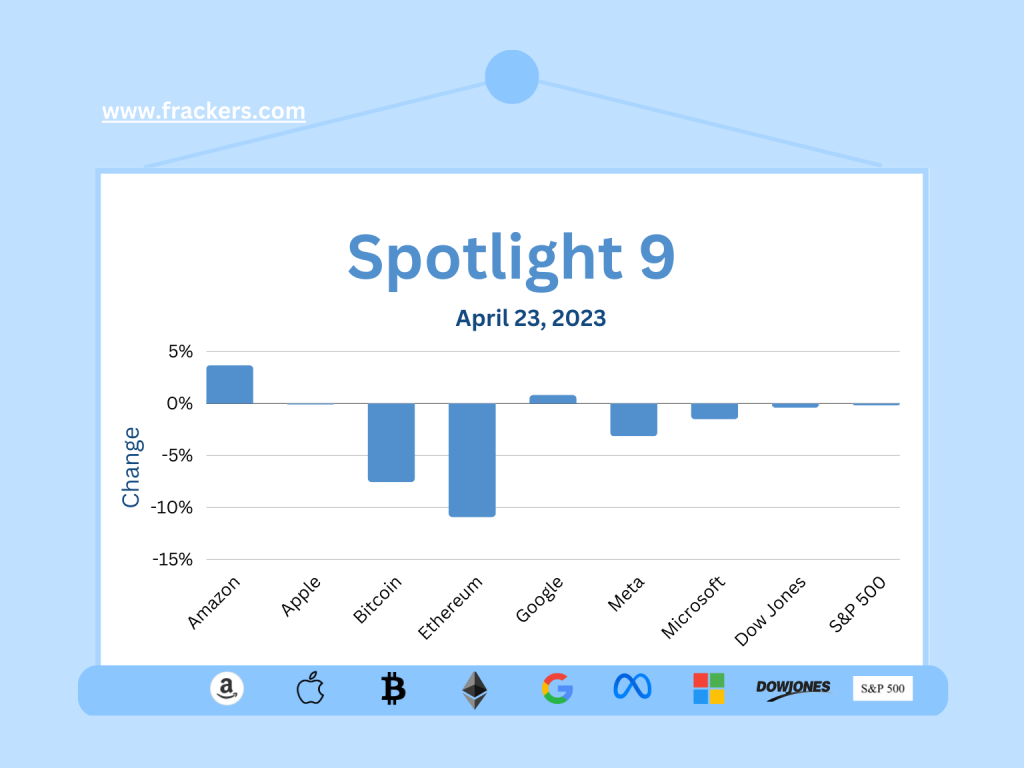

Het beurssentiment bepaalt een groot deel van onze economie en de techsector wordt er zelfs door gedomineerd. De gedachte achter deze portfolio was simpel. Stel, je wilt beleggen, maar niet elke dag aan- en verkopen want dat is tijdrovend en ingewikkeld en je kunt een beetje tegen je verlies; wat koop je dan? Ik heb gekozen voor de 5 grootste techaandelen (Amazon, Apple, Google/Alphabet, Meta en Microsoft) twee indexfondsen (S&P 500 en Dow Jones Index) en de twee grootste cryptocurrencies (Bitcoin en Ethereum). Wie op 1 januari van dit jaar deze negen aankopen had gedaan, elk voor een gelijk bedrag, had vandaag een rendement behaald van 37.6%. Maar vergeleken met een jaar geleden, is het rendement -8%. Dat is het aardige van zo’n portfolio volgen: de duur van de belegging, je investeringshorizon, bepaalt de definitie van succes. Wie alleen naar deze week kijkt, waarin alleen Amazon fier overeind blijft, hunkert naar de oude Zilvervloot-rekening. Overigens lijkt de voornaamste reden dat het aandeel Amazon steeg, de aankondiging dat het bedrijf naast Microsoft en Google ook een voorname rol wil spelen in AI, met Amazon Bedrock als eerste troef. De opzet van Bedrock is interessant, want i.p.v. alles zelf te ontwikkelen biedt Amazon aan AWS klanten de mogelijkheid om AI-modellen te gebruiken van diverse leveranciers, waaronder AWS zelf.

Voor wie meer interesse heeft in AI raad ik je dit gesprek aan, opgestart door NRC-journalist Wouter van Noort die zelf een aantal van mijn favoriete nieuwsbrieven maakt, Future Affairs en Transcend.

Fijne zondag,

-Michiel

Het archief met eerdere nieuwsbrieven staat hier.

p.s. hieronder de conversatie met ChatGPT4 over de rubrieksnaam voor het volgen van een kleine beleggingsportfolio