Doordat ik dit weekend op reis was, heb ik geen goed overzicht van het belangrijkste technieuws. Daarom besteed ik deze nieuwsbrief aan het enige gespreksonderwerp van afgelopen week in techkringen: oprichters of managers — wie zijn beter?

In Silicon Valley ging het afgelopen week vrijwel alleen over ‘Founder Mode’ na een blogpost van Paul Graham, oprichter van ’s werelds meest succesvolle startup-incubator Y Combinator. Graham stelt dat oprichters van startups niet zouden moeten luisteren naar investeerders die vaak aandringen op het aanstellen van ervaren CEO’s en managers, wat volgens Graham vaak desastreuze gevolgen heeft.

Founders of managers?

Opereren in “oprichtersmodus” betekent volgens Graham vasthouden aan de mentaliteit en managementstijl van een oprichter. Het draait om het omzeilen van rigide organisatiestructuren en het bevorderen van nauwe samenwerking tussen afdelingen. Startups in ‘managersmodus’ daarentegen trekken competente, ervaren managers aan om teams te leiden met minimale inmenging van de CEO.

‘De manier waarop managers leren bedrijven te runnen, lijkt op modulair ontwerp, waarbij je subgroepen van het organigram als zwarte dozen behandelt,’ schreef Graham.

Airbnb bijna succesvol de afgrond ingemanaged

Hij was voor het schrijven van zijn blogpost geïnspireerd door een recente toespraak van Airbnb’s medeoprichter Brian Chesky bij Y Combinator. Chesky benadrukte daarin de valkuilen van conventionele wijsheid bij het opschalen van bedrijven, waarbij vaak wordt geadviseerd om goede mensen aan te nemen en hen autonomie te geven. Toen hij dit advies bij Airbnb volgde, leidde dit tot teleurstellende resultaten.

Naar eigen zeggen geïnspireerd door Steve Jobs ontwikkelde Chesky een nieuwe aanpak, die nu lijkt te werken, gezien de sterke financiële prestaties van Airbnb – al zullen bewoners van de binnensteden van Barcelona en Amsterdam daar anders over denken, overspoeld door een golf van rolkoffers en hogere huurprijzen door het ‘succes’ van Airbn.

Veel oprichters in het publiek deelden vergelijkbare ervaringen als Chesky en realiseerden zich dat het gebruikelijke advies hen eerder schaadde dan hielp. Chesky wees erop dat oprichters ook vaak wordt geadviseerd om bij sterke groei hun bedrijven te leiden als professionele managers, wat vaak inefficiënt blijkt.

Apple en Microsoft succesvol in managersmodus

Volgens Chesky en Paul Graham bezitten oprichters unieke vaardigheden die managers zonder ondernemersachtergrond vaak missen. Door deze instincten te onderdrukken, kunnen oprichters hun bedrijven juist schade toebrengen.

Risa Mish, hoogleraar management op Cornell University, stelde daar in Observer tegenover dat juist Steve Jobs met groot succes is opgevolgd door de ervaren manager Tim Cook. Ook Microsoft heeft onder Satya Nadella vele malen beter gepresteerd dan iemand ooit had verwacht.

“Maar het zou zo eenvoudig kunnen zijn als het verschil tussen een team dat nieuwe dingen probeert te creëren en een bedrijf dat zich richt op het laten groeien van bestaande producten en inkomstenbronnen,” aldus Mish.

Voorbeelden genoeg in beide kampen

Mish is blijkbaar vergeten dat Steve Jobs in de jaren tachtig bij Apple werd ontslagen door CEO John Sculley, die afkomstig was van Pepsi Cola en ironisch genoeg door Jobs zelf was gerecruteerd.

De enige innovatie die Sculley bij Apple introduceerde was de legendarische flop Newton, omdat hij niet in staat was het ontegenzeggelijk enorme marktpotentieel van het mobiele apparaat (later juist bewezen door de iPhone) te koppelen aan de juiste timing, de belangrijkste vaardigheid voor een innovatieve CEO. De technologie was nog lang niet klaar voor een apparaat als de Newton; snel mobiel internet ontbrak en de kleine processoren waren nog te zwak.

Voor ik verder afdwaal: tegenover het succes van de managers Tim Cook bij Apple en Satya Nadella bij Microsoft, staat een letterlijk en figuurlijk (cijfermatig en symbolisch) evenredig groot succes in de persoon van Nvidia-oprichter Jensen Huang, die al ruim drie decennia CEO is van de chipmaker die hij zelf oprichtte.

Ook zullen aandeelhouders van Salesforce geen tranen met tuiten huilen dat oprichter Marc Benioff daar al ruim een kwart eeuw de leiding heeft en volgens The Information zelfs bezig is aan een comeback, voorzover nodig. Kortom: of het gaat om succesvolle founders of succesvolle managers, in beide kampen is de keuze reuze.

Cijfers tonen aan: oprichters presteren beter

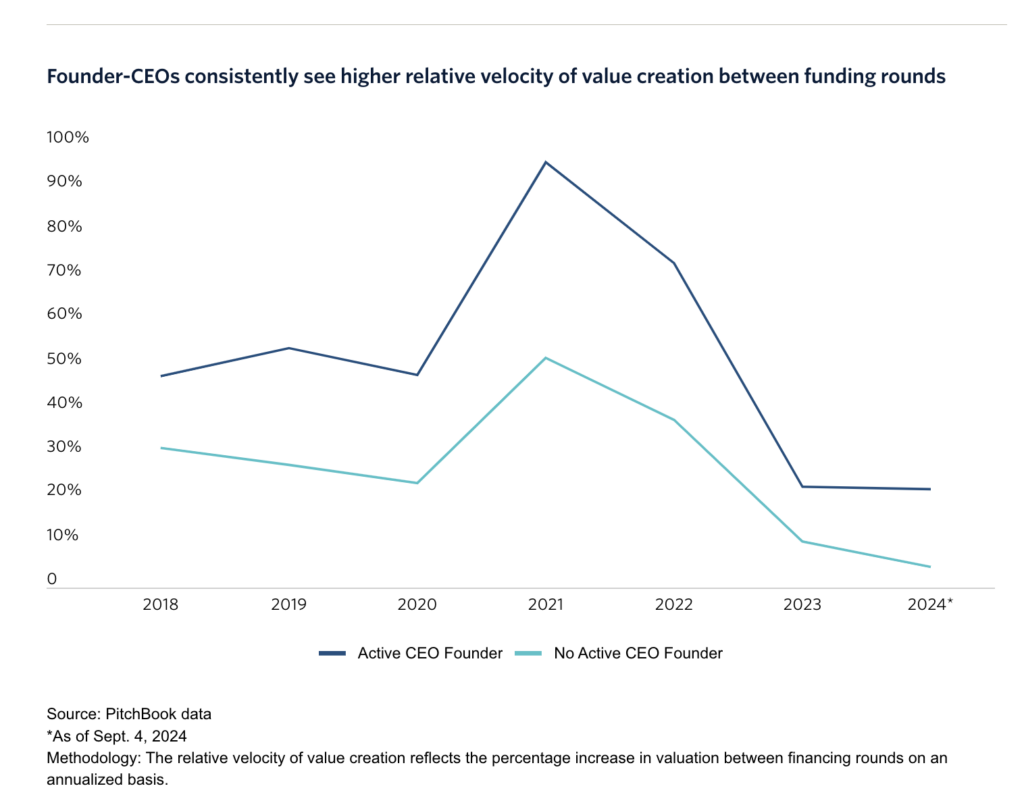

Gelukkig is het dilemma inmiddels kwantitatief onderzocht en blijkt dat Paul Graham’s stelling klopt: de oprichtersmodus is vaak superieur als het gaat om waardecreatie, volgens een analyse van PitchBook-gegevens.

Pitchbook concludeert:

“In elk van de afgelopen vijf jaar groeiden door VC gesteunde bedrijven onder leiding van een oprichter aanzienlijk sneller in waarde dan bedrijven onder leiding van niet-oprichters. Dit jaar bedroeg de relatieve snelheid van waardecreatie voor oprichter-CEO’s 22,4%, tegenover 4,7% voor niet-oprichter-CEO’s.

In de gekozen methodologie weerspiegelt het cijfer voor relatieve snelheid het percentage van de waardestijging tussen financieringsrondes, uitgedrukt op jaarbasis. Onder de bedrijven die dit jaar financiering ophaalden, was de mediane waardegroei $3,6 miljoen hoger onder oprichter-CEO’s.

Volgens Graham zijn oprichter-CEO’s van snelgroeiende bedrijven vooral ‘wendbaarder’ dan professionele CEO’s. Die detail georienteerde aanpak kan leiden tot hogere groei door verbetering van het product, of door frontlinie werknemers beter te motiveren.”

Kwetsbare bedrijven hebben ondernemers nodig

Kwetsbare bedrijven hebben ondernemers nodig. Naar mijn mening, die gebaseerd is op ervaring en observatie, maar niet ondersteund wordt door kwantitatief onderzoek, moeten bedrijven die ongeacht hun leeftijd voornamelijk afhankelijk zijn van één product of één inkomstenbron, bij voorkeur een oprichter aan het roer hebben.

Neem Google, dat momenteel onder druk staat door de opkomst van OpenAI met ChatGPT, terwijl hun omzet grotendeels afkomstig is uit advertenties, met name via de zoekmachine.

Zodra de zoekmachine minder verkeer genereert, zal de omzet dalen, en wordt het voor Google erg lastig. CEO Sundar Pichai is duidelijk een bekwame manager, maar de komende jaren zullen uitwijzen hoe goed hij is als ondernemer.

We hoeven alleen terug te denken aan de tijdelijke successen van Nokia en Blackberry om te zien wat er gebeurt als bedrijven die leunen op innovatie worden geleid door managers, die niet in staat zijn hun producten aan te passen wanneer ze frontaal worden aangevallen.

De flexibiliteit van Zuckerberg

Een uitstekend voorbeeld van een relatief jonge oprichter die het vak beheerst, is Mark Zuckerberg. Toen Instagram een bedreiging bleek te vormen voor Facebook, kocht hij het snel voor een miljard dollar. Een bedrag waar velen de wenkbrauwen bij fronsten, maar insiders wisten dat het een koopje was. WhatsApp was ongeveer twintig keer zo duur, maar nog steeds een goede deal.

Toen Snapchat met Stories een grote bedreiging vormde voor Instagram, liet Zuckerberg Instagram eenvoudigweg de volledige functionaliteit van Snapchat kopiëren, zonder ego. Dit redde Instagram. Momenteel probeert hij iets soortgelijks in reactie op TikTok.

Ik ben ervan overtuigd dat een klassieke manager nooit Instagram en Whatsapp had gekocht of Instagram zo snel had laten reageren op de concurrentie van Snapchat en TikTok. Dat Zuckerberg inmiddels tientallen miljarden heeft weggepist aan onduidelijke Metaverse-avonturen, is daarbij vergeleken een afronding na de komma.

Conclusie uit dertig jaar als ondernemer en investeerder

Het is interessant dat veel succesvolle ondernemers zeggen jarenlang te worden begeleid door een kleine groep ervaren adviseurs die hun vertrouwen geniet. Zo was ex-Intuit CEO Bill Campbell, over wie het uitstekende boek Trillion Dollar Coach is geschreven, een beroemde adviseur van ondermeer Steve Jobs en de oprichters van Google.

In Silicon Valley zijn investeerders en ex-ondernemers Reid Hoffman, Peter Thiel en Marc Andreessen veel genoemde namen. Juist in de combinatie ondernemerservaring en investeringservaring blijkt van unieke waarde te zijn.

Dit onderwerp ligt me na aan het hart omdat ik, na bijna tien jaar als werknemer tijdens mijn school- en studententijd, vijftien jaar ondernemer ben geweest en sindsdien vijftien jaar investeerder en adviseur.

Coachbare gekken

Mijn conclusie is dat coachbare ondernemers de grootste kans op succes hebben.

Eén van de voordelen van eerst werknemer zijn geweest, is dat ik vooral heb geleerd hoe ik als werkgever in ieder geval niet met mensen wilde omgaan. Tijdens mijn tijd als jonge ondernemer bij Planet Internet heb ik echter enorm veel steun gehad aan waardevolle adviezen, zowel van ondernemers als van managers.

Achteraf realiseerde ik me pas hoeveel geluk ik had dat ondernemers zoals Eckart Wintzen (BSO) en Maarten van den Biggelaar (Quote Media) de tijd voor me namen, net als leden van de Raad van Bestuur van de Telegraaf en Ben Verwaayen van KPN.

Het ontging me niet dat Quote, Telegraaf en KPN aandeelhouders waren, en dat perspectief uiteraard altijd meespeelde. Maar dat doet niets af aan de kwaliteit van hun adviezen.

Later zag ik als adviseur bij hetzelfde Quote Media en bij dancebedrijf ID&T hoe talenten zoals Jort Kelder en Duncan Stutterheim naar de buitenwereld misschien stronteigenwijs leken, maar in de praktijk juist op cruciale momenten heel goed luisterden naar adviezen – en vervolgens, zoals het hoort, hun eigen beslissingen namen.

Moeilijker werd het in constellaties waarbij er juist veel verschillende winden waaien, zoals ik meemaakte bij de OV Chipkaart: een consortium van OV-bedrijven die onderling concurreerden, dat een aanbesting deed bij een consortium van bedrijven die op hun beurt onderling concurreerden… kortom, het liep als een trein. Een NS-trein, welteverstaan.

Bij de Silicon Valley-startup Jaunt ervaarde ik iets vergelijkbaars. Deze virtual reality-pionier had binnen zowel het team als de investeerders een mix van techneuten en mediamensen, een ware fusie tussen Silicon Valley en Hollywood.

Zowel camera’s maken als VR-producties, kantoren in Palo Alto en Santa Monica en aandeelhouders die varieerden van de traditionele winstbeluste Silicon Valley vc-fondsen, tot Disney en Sky; ofwel ook nog eens Amerikaanse, Europese en Chinese aandeelhouders. Je eindigt met een soort prakje van nasi en zuurkool, of een pizza met gember en boerenkool. Los van elkaar uitstekend, maar de combinatie werkt niet. Er ontbreekt focus en een eenduidige denkrichting, die een goede oprichter als CEO wel heeft.

Dat is een lange aanloop naar mijn conclusie: de beste CEO’s zijn oprichters die maniakaal zijn in hun visie, maar wel coachbaar in hun uitvoering; noem het coachbare gekken. En dan bij voorkeur coachbaar door zowel ervaren founders *en* managers.

Dank voor je belangstelling en tot volgende week!